Even so, observers are divided about Apple’s strategy and distribution method. The most popular theory is that Apple’s programming will be available as a subscription service, at some unspecified price, and possibly bundled with other Apple subscriptions. This is by far the most discussed by analysts, the entertainment and technology press, and commentators. Others haveargued that Apple will offer a free service to boost Apple TV hardware sales. Both of these theories suggest Apple can either increase its service revenue or offer free content to strengthen its hardware ecosystem.

Recently, a different theory has emerged, arguing that it’s possible for Apple to increase its service revenue, while also offering its original programming for free. By offering free programming, Apple will encourage the users of its 1.4 billion active devices to use its TV platform by default, then purchase more subscriptions with Apple. If that works, Apple will increase its overall television service revenue without competing in a brutal SVOD landscape, and increase Apple TV hardware sales at the same time. Those are two large and unique sources of growth.

This theory has not yet reached a critical mass. The best source I could read was a CNBC article which provides an outline of the idea with quotes from anonymous Apple sources. The Information publishes rumors that suggest either a paid or free service. Media analyst Rich Greenfield (follow him on Twitter) has written a blog post, but it’s only available to corporate clients. In my view, it’s the strategy that’s most likely to succeed, so I’ve written my own basic analysis.

This report explains why the most established theories don’t add up, how a better model would work, and what that means for Apple and the industry.

The established theories, and why they don’t sound right

1. Apple’s originals will be available for a subscription fee (the service revenue theory)

Tim Cook is clearly interested in building service revenue, and given the success of Netflix and Amazon Prime, the idea that Apple would join the market with a similar television subscription service seems to makes sense. The theory goes that Apple’s originals will be available as part of an SVOD service, where customers pay a recurring fee. The service will either be available on its own or bundled with other Apple media services like Apple Music, maybe iCloud storage and/or its rumored news and games services. Apple creates a media-focused competitor to Prime, directly increasing its service revenue.

The problem is that Apple is joining the market late. Netflix has 137 million subscribers and feels confident enough that it can charge more without a significant number of them leaving. Prime is at 100 million globally, with a rumored 26 million US subscribers watching video. Hulu’s at 23 million and only operates in the US, but there’s a Hulu in several crucial markets (e.g. the UK’s Now TV, which promotes itself as an on-demand service, and Australia’s Stan), and niche competitors as well. Apple was late to music streaming and is doing well, but Spotify only owned a small market in 2015. The streaming video market is already much larger.

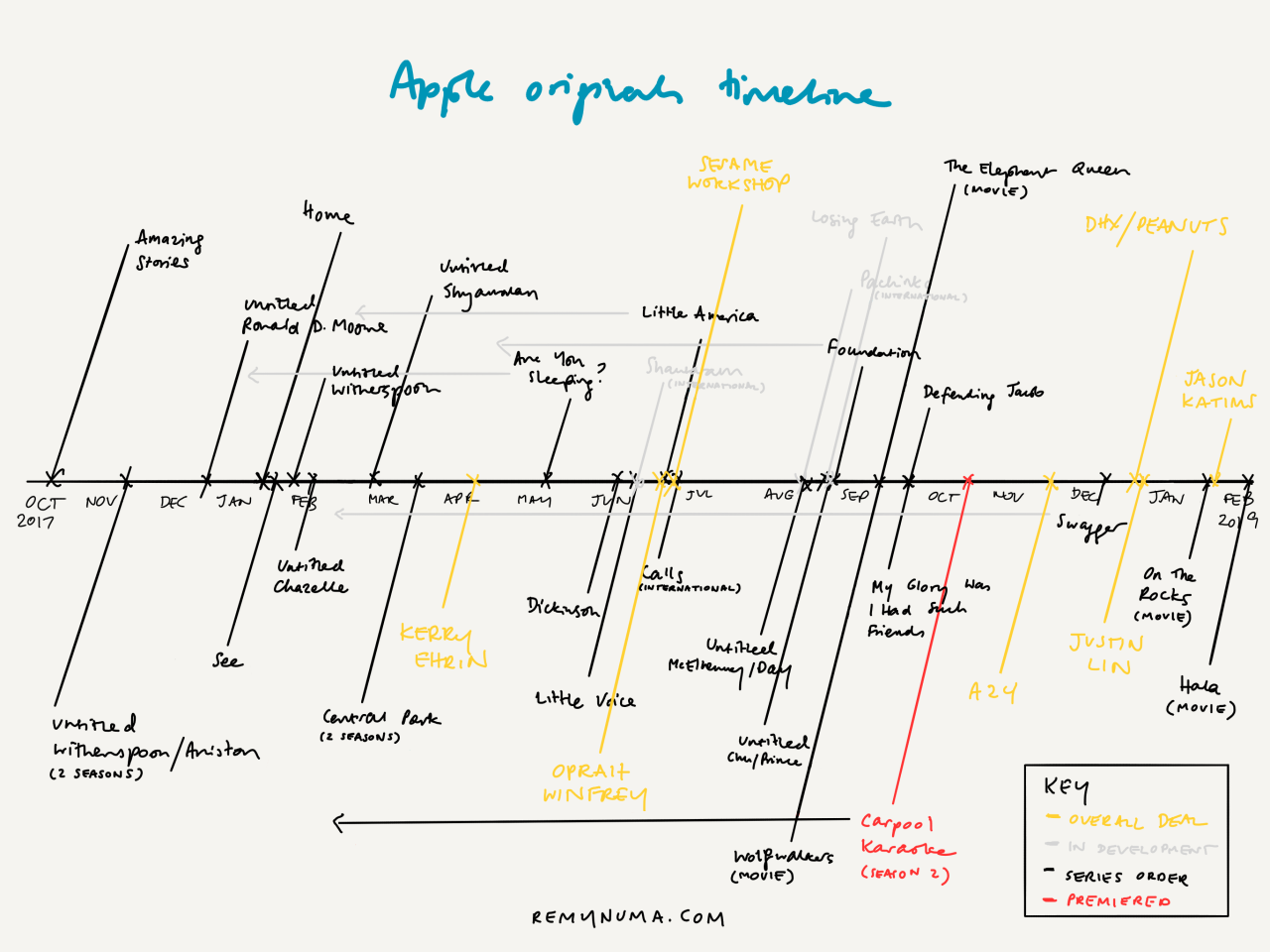

Even if that weren’t an issue, Apple’s investment looks different to the dominant SVOD services. First, at the rumored $1 billion per year, Apple is investing much less in original productions than its competitors. Netflix spends $13 billion, Amazon spends $5 billion, and Hulu spends more than $2.5 billion. There are rumors that Apple’s investment is higher than $1 billion, and given the deals they’re signing with everyone from Justin Lin to A24, it probably is. But consider the projects that Apple has confirmed so far:

Apple will have far fewer titles to offer than its competitors. The company is announcing ~1-3 projects per month, so we can assume a similar release schedule. That puts Apple’s schedule in the same league as Prime and Hulu for original series, but nowhere near Netflix. It also won’t have any of the original productions that are already available on all three services. In Netflix’s case, that’s 700+ series and 200+ movies, while Prime and Hulu have 100+ original titles to offer in total.

At launch, the originals issue is more complicated. Apple won’t want to release any of its original series simultaneously, because doing so would waste months of free publicity and promotion for each series. With only one original title to offer (Amazing Stories started shooting in December and the Witherspoon/Aniston project joined a few weeks later, so it will probably be one of those), it’s hard to imagine subscribers choosing to take up a $10ish subscription, or a much more expensive Apple bundle.

Netflix, Prime, and Hulu all started with one original series, but they boosted the extensive libraries of acquired content that each service has offered since its inception. If Apple had a large library to debut with its service, then the lack of originals would matter less, but Apple hasn’t acquired a studio or made a deal to distribute any movies or television series that have already premiered elsewhere. There’s nothing to indicate that they’re on the verge of taking those steps.

I can’t see a pathway where Apple only offers its original programming in a paid service and/or bundle. It’s possible that Apple will offer additional benefits to subscribers of an ‘Apple Prime,’ like 4K streaming or the ability to watch every episode at once, but that’s a messy product strategy.

2. Apple’s originals will be free (the unit sales theory)

Apple wants to own the living room, and Apple TV sales are crucial in achieving that goal. Recent data suggests that Apple is doing well with 4K TV owners, but in the overall market, Apple lags behind products from Roku, Chromecast, and Amazon. In order to increase its share, Apple can either launch new products (which they’re apparently doing) and/or invest in advertising. One great way to advertise is with exclusive programming.

The idea is that Apple would release its originals for free through the Apple TV app, which is already available on iPhone, iPad and the Apple TV. Viewers can watch the show on their personal iOS devices, but if they want to see them on a big screen, they’ll need the Apple TV hardware. As each original is released, Apple gets another opportunity to tell a large, global viewing audience that the Apple TV is the only place to enjoy its buzzy new shows, and an increase in hardware sales should follow.

A free service would eliminate budget and content acquisition issues. Just about everyone with an iOS device has an Apple ID, so getting new users into the TV app on iOS won’t require a large content library. As for purchasing an Apple TV, the more originals, the better the chance that the strategy works, but Apple will be releasing shows frequently enough that consumers could reasonably feel like the investment is worthwhile.

This plan is logical, but incomplete. First, $1 billion+ is a lot of money to spend to advertise one device in Apple’s ecosystem. Apple spent $1.8 billion total on advertising in 2015, and while that number will have grown, the iPhone is likely draining most of that budget. Second, while AirPlay is not a substitution for the Apple TV, if Apple’s goals with television were only to increase hardware sales, it would be counterintuitive to launch AirPlay on a range of other devices, which Apple did three weeks ago. Finally, Cook says Apple is thinking about television as a service, which is incompatible with this approach.

A better strategy: increase overall service revenue with free original programming

The conventional wisdom is that Apple must charge a subscription fee for its original programming in order to increase its service revenue. But as the video streaming market grows, Apple has an opportunity to take a cut from users’ subscriptions to many third-party video services. That’s a better strategy than joining the SVOD market because it’s more closely aligned with Apple’s long-term goals.

Apple already earns subscription revenue from TV services

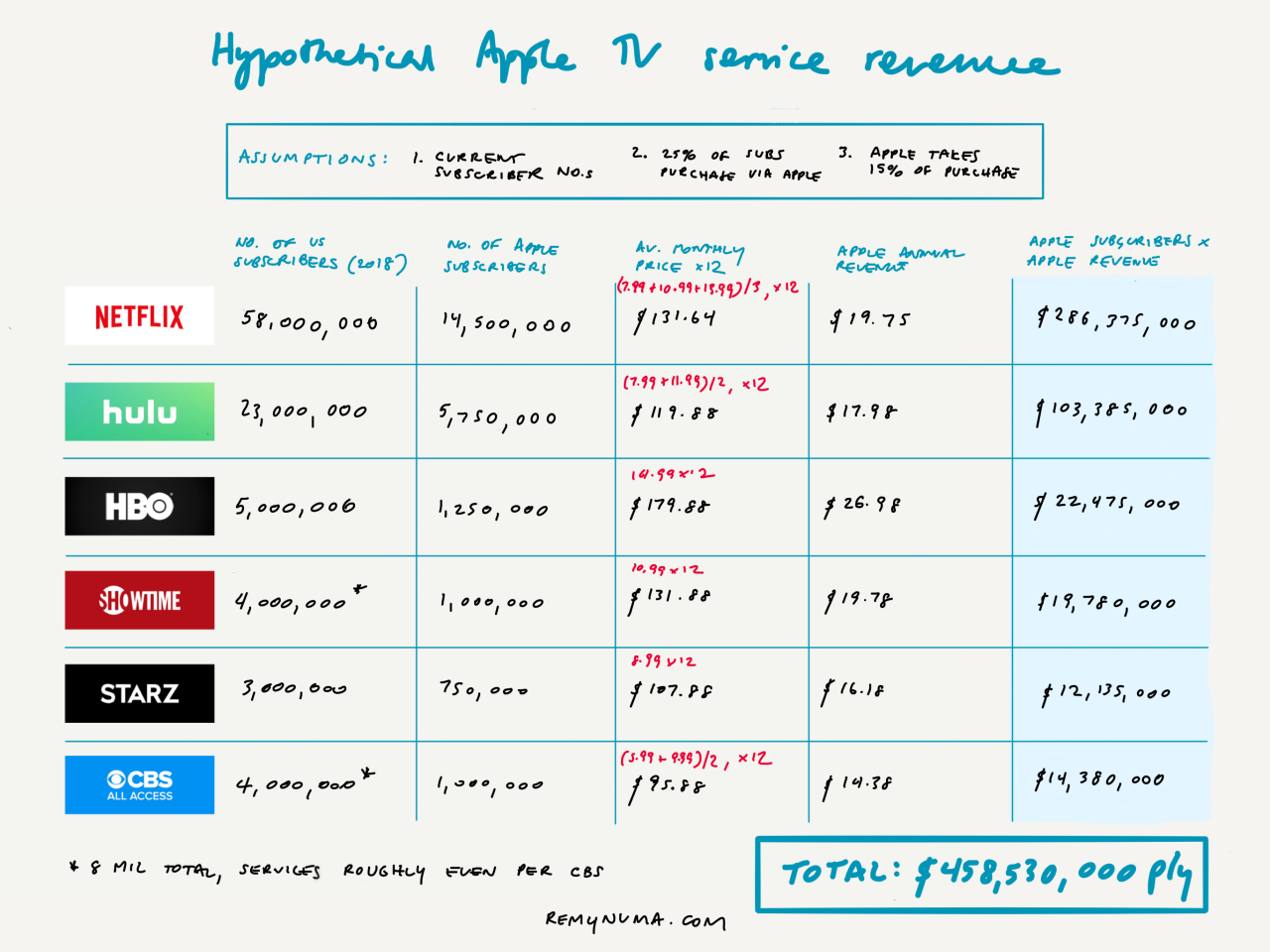

Apple currently offers the ability to purchase subscriptions to TV services via in-app purchases on the App Store. The list of services includes Hulu, Prime Video, HBO, Showtime, Starz, ESPN+, CBS All Access, AMC Premiere, and Fox Nation, along with cable bundles like Fubo, the ad-free version of YouTube, and a raft of niche TV products. Netflix stopped offering in-app subscriptions this month, but Apple is still collecting revenue from existing users there, too. For each service, Apple says it takes 30% of the subscription price in the first year, and 15% thereafter, but for the major services, it’s more likely that Apple is simply taking 15% from the beginning.

It’s impossible to say how much revenue Apple is making from video subscriptions, except that it’s a driver of their $10.88 billion in service revenue last quarter. But for the sake of argument, let’s do some very rough back-of-the-envelope math. If you use current subscriber numbers for six large standalone services on the App Store, assume that about 25% of those subscribers are doing so through Apple, then take a 15% cut from the average subscription price, you end up with a lot of money:

Again, this is a rough analysis. I’m generously assuming, for example, that Netflix sells all three plans in equal proportions, and that 25% of users across all six services have subscribed through Apple. Those assumptions are almost certainly wrong. I’m including the numbers here merely to give you a sense of how quickly that 15% cut adds up. In this scenario, Apple’s earning approximately $0.5 billion in annual revenue, in the U.S. market, excluding heavy-hitters like YouTube and ESPN. The global figure, including all services, will easily add up to over $1 billion.

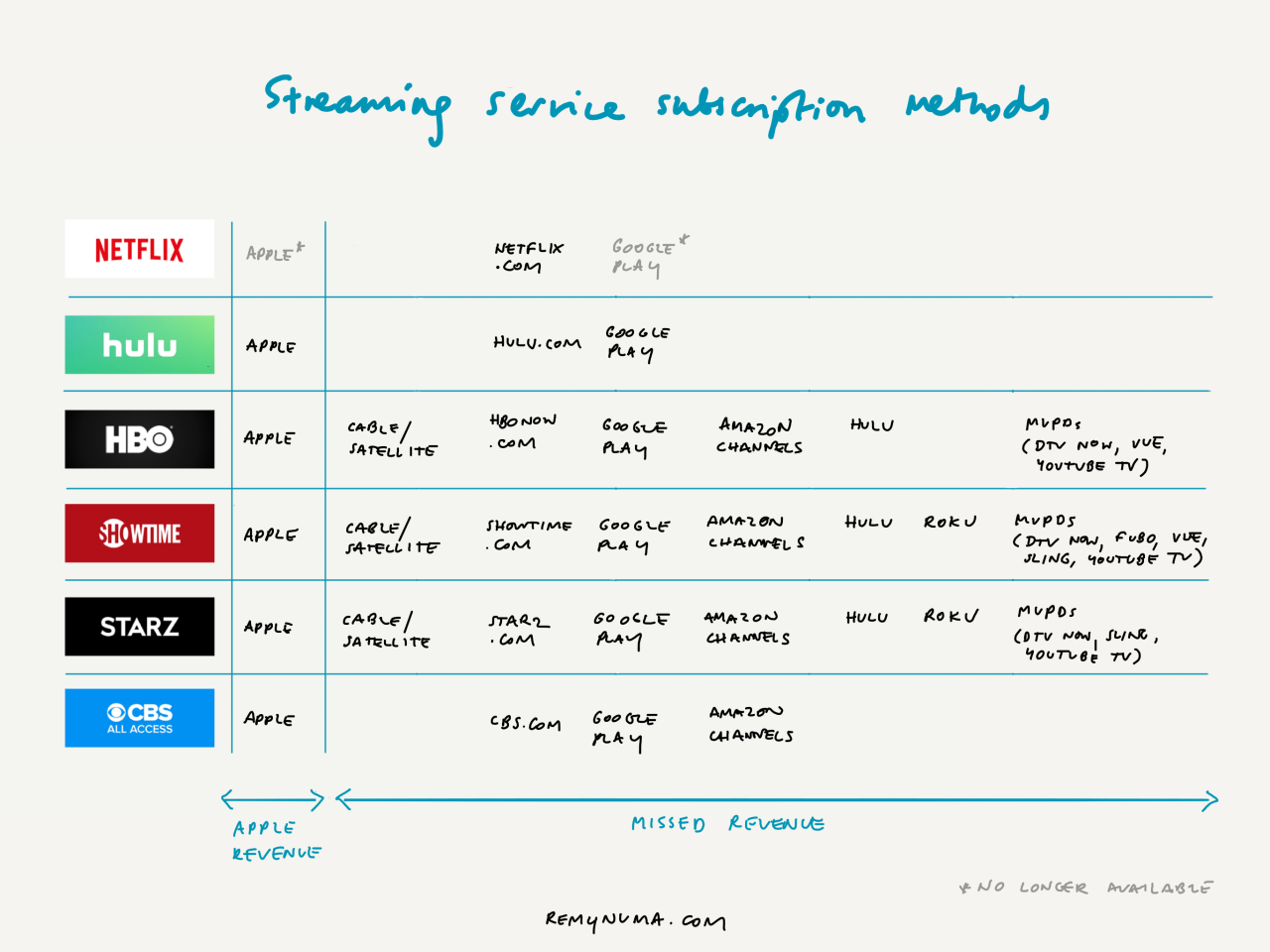

Even with that wide range of services and an enormous user base, Apple remains just one of many companies offering users subscriptions. Here’s the range of purchase methods for the same six services:

Every time a user purchases a subscription through one of the non-Apple platforms shown above, Apple is missing out on service revenue. At a hypothetical $1 billion+ in annual revenue for 25% of all users, Apple stands to earn billions more depending on its market penetration. To be clear, no matter what Apple does to increase its subscription revenue, it will struggle to reach users in the Google or Amazon ecosystems. But that still leaves a lot of people who either don’t subscribe to these services now or purchased them through a provider like Hulu or DirecTV Now.

The SVOD market is about to grow dramatically

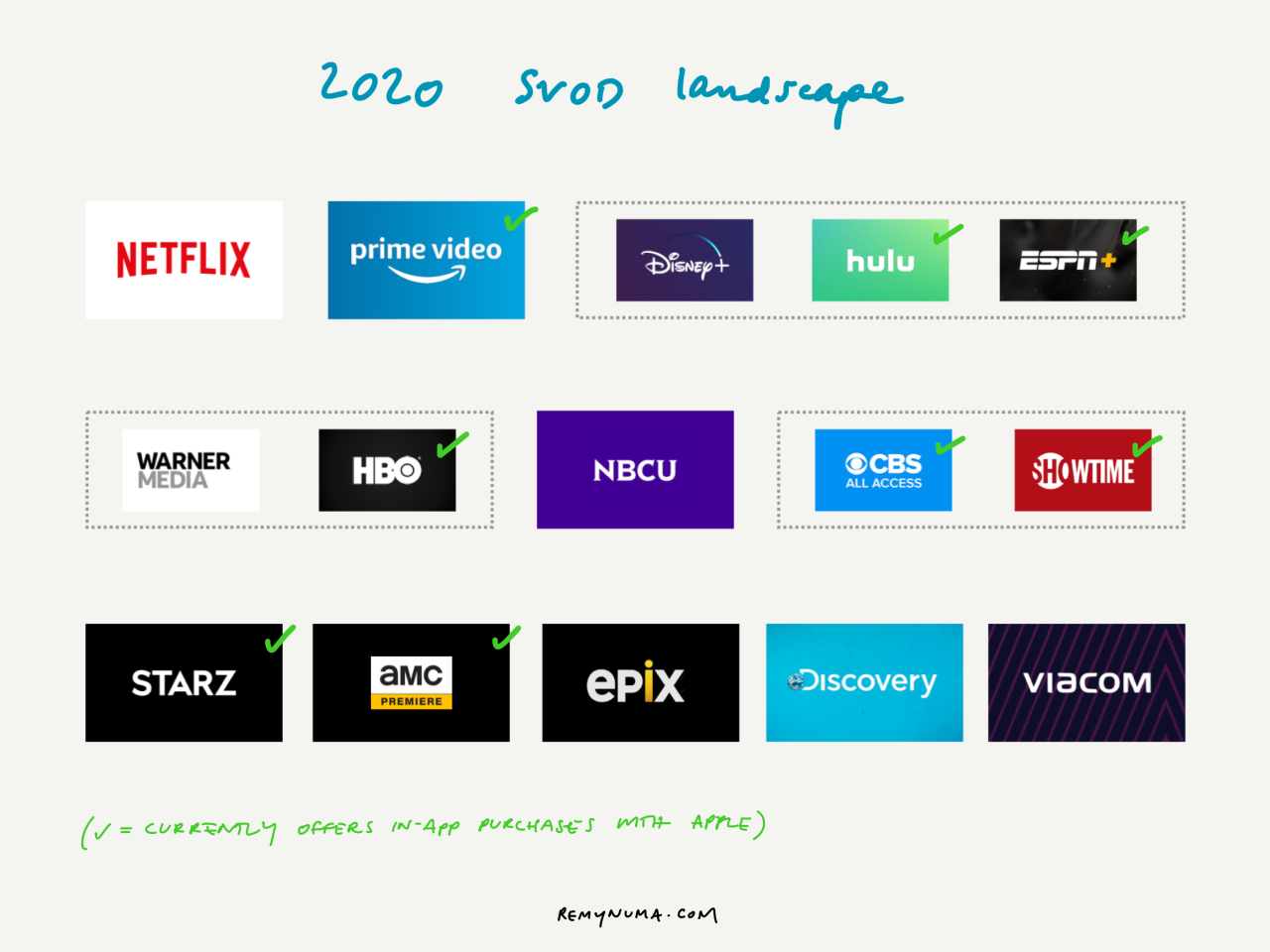

Apple’s television service revenue opportunity is about to get significantly larger. Disney and Warner will launch fully-fledged global SVOD products by the end of the year. NBCUniversal is still married to cable, but it will offer a direct-to-consumer option in the US and Europe by the end of next year. AMC Premiere requires cable, but its parent company has experience with niche SVOD services. And both Viacom and Discovery are considering launching their own offerings. Put it all together with the existing range of services, and you get a crowded US entertainment landscape:

If Disney, Warner, and NBC are all serious about competing with Netflix, and assuming they agree to a 15% cut from Apple, then Apple’s global television service revenue will skyrocket. It’s likely already at over $1 billion per year, so the potential earnings from existing SVOD subscribers are worth fighting for.

Remember that there are also 93.8 million homes in the U.S. and 69.2 million homes in Europe with a traditional cable television subscription. When the cable bundle crumbles, those subscribers will still want a way to watch movies and television. They’ll add more services to fill the void.

In short, Apple’s revenue opportunity is enormous.

Apple is building a TV supermarket

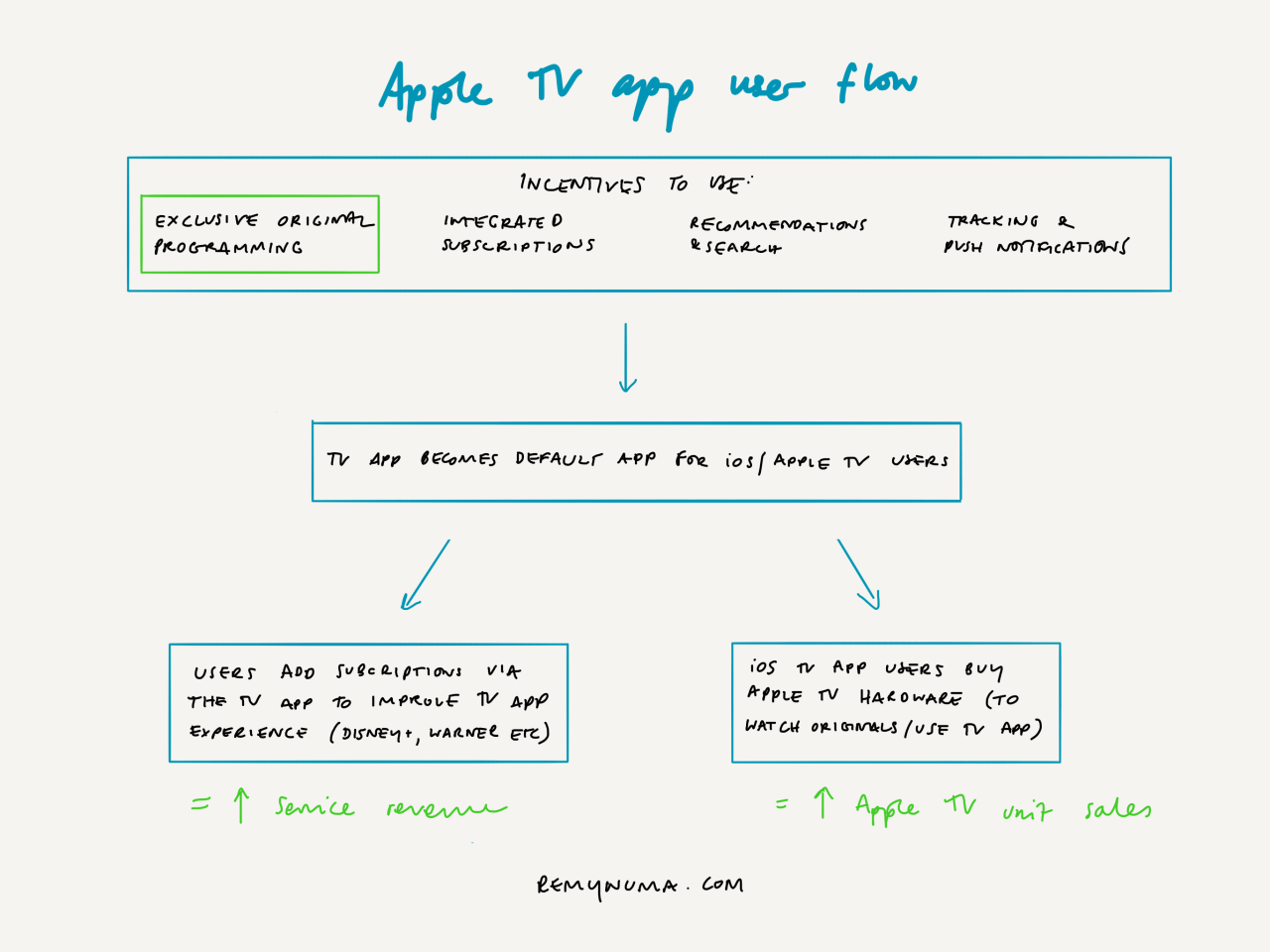

Apple can take further advantage of the impending TV landscape by making it as easy as possible for its users to sign up for more subscriptions. That’s exactly what it’s doing with the Apple TV app.

The Apple TV app already offers a compelling all-in-one experience. The app allows users to find and track movies, TV series, and sports across all of the major SVOD, cable, and free video apps available on iOS and Apple TV, except Netflix. Apple provides curated recommendations to help users discover new shows across those services. In the clearest indication yet of Apple’s originals strategy, it is also the home of Carpool Karaoke, an unscripted series which moved from Apple Music after its first season.

The TV app is widely available. It’s preinstalled on every iPhone, iPad and Apple TV running iOS 10 and up in ten countries. Apple doesn’t say how many users have the app installed, but they serve 1.4 billion active devices, 900 million of which are iPhones. Even when making conservative guesses about the number of active iPads and Apple TVs, iOS adoption rates, and the number of users in those territories (let’s call it 30%), you end up with a ballpark of 300 million devices. Apple has a strong start in television streaming.

Apple also has stronger relationships with its partners than similar products. Its most direct competitor is Amazon Channels, which offers subscriptions and playback directly in its Prime Video apps. Apple’s advantage is that it integrates recommendations from Hulu, cable services, and a wide range of free apps, including the major free networks in key markets, but that advantage will dissipate as Amazon continues to pursue its strategy. Meanwhile, Google also offers in-app purchases through its app store, but is yet to offer an integrated TV experience. It’s stuck in cable land with YouTube TV, which performs well with users looking for a cheaper live TV package, but is hovering around 1 million subscribers.

The future of the Apple TV app

For Apple’s TV aggregator to work in the long run, it needs to persuade new partners that integrating with the TV app will grow their businesses. In particular, Apple needs to show Disney, Warner, and NBCU that it’s providing value in exchange for a 15% cut from every subscription. Apple’s best case is that it promotes programming from a wide variety of sources, then offers a simple way to subscribe to them. Most Apple TV app users already have credit card information stored with Apple, so signing up for a new subscription takes less than 30 seconds. Convincing the studios is a big challenge, and I wouldn’t be surprised to see at least one of the major services circumvent Apple’s business model. But Apple has a compelling product to offer its partners, all of which are looking for ways to reach a large subscriber base quickly.

In the current iteration of the app, adding a subscription for a video service is somewhat indirect. Users select an episode, leave the TV app, download the third-party app, sign up for an account, confirm a subscription with Apple, then use the third-party app’s menu to select the episode again. In total, it’s a nine step process.

Apple can reduce that complexity by:

eliminating the need to purchase a subscription within the third-party app

integrating video playback into the TV app.

Ideally, users should only need to find an episode, select the service, confirm the price, then start watching. That’s a much quicker process to follow:

Reducing the friction between selecting an episode and watching it will encourage more users to subscribe to more services.

In addition to integrated subscriptions and playback, Apple has a range of options to improve the TV app experience:

Overall ease of use: The TV app’s ability to tracks programming across many sources also makes it more complex. Users will often find that a series is available on several services, each with a different price point. Some shows are only available with cable, some can only be purchased through iTunes. Apple’s deal with Amazon is also confusing: many shows appear to be available on Prime Video, but only with an add-on that can’t be purchased with Apple. All of these concessions make a platform like Netflix the simpler and cheaper option for many, and that’s a huge threat to Apple’s strategy. Apple needs to fix this to thrive.

Mac support: the TV app doesn’t work on macOS, a platform that millions of SVOD subscribers use to watch videos. With no native apps for Mac from any of the services, solving this problem will take years. Apple can either aggressively pursue native app development once it launches Marzipan or give up and go to the web.

Personalized recommendations: a job for John Giannandrea. A recommendation algorithm would help Apple target new shows to users just like Netflix does. Apple has already implemented a similar feature with its weekly Apple Music mixes, so it’s likely developing a similar feature for TV.

Bundled subscriptions: Apple is participating in the downfall of the cable bundle, but consumers still want ways to pay less for a wide range of programming. Apple could work with TV services to offer discounted bundles. That proposal is particularly likely to appeal to companies like AMC and Starz, which don’t have the same content volume and marketing budgets as the major studios.

Cross-service autoplay: if Apple can convince third-party services to allow playback within the TV app, then it would also have the ability to automatically play content from different services at the conclusion of a movie/show. That would help TV services attract and retain users who are unfamiliar with their content.

Free programming: the major services all provide free trials to new customers, but Apple could also offer selected episodes from third-party services for free. Combined with cross-service autoplay, this feature would be a powerful aid for services looking to attract new users.

Some of the proposed new features above, like tighter integration of subscriptions and free programming, should be reasonably easy to pull off, and recent reporting suggests that Apple is alreadyworking with the major services on that move.

Integrated playback and/or cross-service autoplay are much bigger asks. There is some precedent: cable viewers and users of streaming platforms like Hulu and Amazon Channels can view programming from HBO, Showtime, and/or Starz directly within those platforms’ apps and alongside other content. For example, a Prime user with Showtime can watch Homeland within the Prime app, then see a recommendation for Amazon’s Jack Ryan. But persuading the studios to do the same, especially when they are all investing billions of dollars into streaming technology and content recommendation algorithms, is going to be a much more difficult task.

Apple will benefit from implementing any one of the features suggested above, and its best argument in persuading partners to accept the changes is also the TV app’s biggest weakness: Netflix will not be part of it. Netflix’s lack of participation has been a big problem for user adoption so far, and will be a big drag on revenue in the future. But Apple can tell Netflix’s competitors that by including their service in the TV app, Apple will give users a better selection of programming than Netflix ever can, encouraging users to subscribe to Netflix less frequently or abandon it.

To be clear, I don’t think Apple has an objection to Netflix’s success. In the revenue analysis above, Apple already takes hundreds of millions of dollars from Netflix subscribers who signed up before it stopped offering in-app purchases. Re-integrating with Apple’s subscriptions platform would improve that figure. Nonetheless, without Netflix’s participation, Apple will find it easier to persuade competitors to get on board.

Original programming is the supermarket’s loss-leader

With integrated subscriptions and the new features discussed above, Apple is building an impressive TV supermarket. The next step is to get more users to walk through the front door. That’s where original programming comes in.

Experienced executives: Apple hired Jamie Erlicht and Zack Van Amburg, two seasoned development execs previously responsible for Breaking Bad and The Crown, instead of handing new responsibilities to its current team.

A-list talent: Apple has acquired projects from Steven Spielberg, Reece Witherspoon, Damien Chazelle, Oprah Winfrey, and Kevin Durant, some of whom are making their television debuts. It’s also bringing stars like Jennifer Aniston and Steve Carell back to television for the first time in over a decade.

Global development: Apple hired Morgan Wandell last year to oversee its international efforts, and that’s culminated in deals to develop programming from India, Japan/Korea, France, and Ireland.

Those moves all point to programming that will attract a wide and global audience. By offering originals that can be watched by anybody, Apple gets the best possible opportunity to persuade users to start with the TV app ahead of any other service. This isn’t because of some cultural aversion to adult themes (Apple Music offers a ton of uncensored content to paid subscribers) but it doesn’t make sense to focus on the same type of programming that airs on HBO when you’re pushing shows to 300 million devices. Apple’s partnerships with HBO and other third-party services ensure it has edgier content for viewers who want it.

The distribution method is already clear. As mentioned above, Apple releases new episodes of Carpool Karaoke every Friday on the Apple TV app. Apple sends push notifications to TV app users to alert them about new episodes, which are available within the app itself. The show is free to watch, as long as you have an Apple ID. Episodes are ad-free and available in up to 4K resolution. Apple might change some of those variables when it launches its scripted programming, but Carpool is a solid demonstration of the basics.

Original programming is the final piece of the puzzle in Apple’s overall strategy:

With four big incentives to use the service and a goal to make the TV app the default viewing experience for users in its ecosystem, Apple will hope for two outcomes: more service profit, and more Apple TV unit sales.

Outcome #1: Apple increases service profit

Apple can expect to increase its service profit, primarily because it will continue to take a substantial cut from subscriptions. It won’t deal with the same challenges as SVOD providers, who have higher costs and more competition.

1. Increase service revenue

Apple’s quest for service revenue leads many to believe that Apple’s originals won’t be free, but the two concepts aren’t mutually exclusive. By taking a 15% cut from every subscription (even a lower cut would suffice), and encouraging users to take up more services when new companies enter the market, Apple can expect to see its overall service revenue rise.

There’s too many variables to make an informed estimate of Apple’s potential earnings, but consider Apple’s position on a per user basis:

In this hypothetical, where User A takes just one major service consistently and samples two lower-priced services throughout the year, Apple makes more revenue than those two. That’s a great outcome for a company that isn’t directly competing in the SVOD landscape.

2. Avoid SVOD challenges

Service X may take the highest amount of revenue in the scenario above, but it also has the highest costs. In fact, any major service competing for paid viewers will need to spend invest more than Apple to survive. In the existing landscape, Netflix, Prime, and Hulu are spending a combined $20.5 billion per year on content, and that’s before you consider Disney, Warner, and NBCU. Apple’s services profit will increase not just because it’s taking a cut from TV companies, but because it’s not spending as much as they will.

Even if all of the services can afford to invest in programming, they’re going to compete in what will start out as an enormous field. Apple is wisely choosing not to become yet another competitor in that landscape:

As a subscription competitor, Apple would spend more and make less, all because it went after the same growth that Netflix has already achieved. As a subscription platform, it takes unique advantage of its strong ecosystem, and sets itself up to survive even when other streaming services fail.

Finally, by staying out of the SVOD business, Apple won’t be subject to the same revenue fluctuations that TV companies will. As more services launch, many users will switch between services to keep their budgets consistent. Returning to the revenue diagram above, when User A drops Service Y in favour of Service Z, it’s a major problem for Service Y, which needs revenue to stay in business. Since Apple takes revenue from Service Y and Service Z, it takes a minor hit in Month 3, but it collects either way.

Outcome #2: Apple strengthens Apple TV unit sales

Apple’s TV app is likely to remain available exclusively on the Apple TV. It still makes a lot of strategic sense to offer high-budget and highly-anticipated entertainment on your own platforms, and Apple can expect to see a rise in Apple TV hardware sales by making that programming exclusive. It would also be impossible for Apple to offer features like integrated subscriptions and episode tracking on any other platform.

To a lesser extent, originals will boost the entire Apple hardware ecosystem. iOS users may not subscribe to other platforms or buy an Apple TV, but they’re still getting a sizable collection of free exclusive programming. That gives them another reason to stick with Apple, and Android users a small incentive to switch. Again, Apple’s challenge is to find a way to bring the TV app to the Mac, but iPhone, iPad, and Apple TV sales will all be aided by this approach.

Conclusion

How do you get rich in a gold rush? You sell pickaxes. Netflix, the film studios, and all their niche competitors can try and strike it big, but if Apple is able to carry out the ambitious strategy that’s detailed in this report, it has the potential not only to fulfill its service revenue mandate, but establish itself as a powerful gatekeeper in the TV market. That’s the best possible outcome for Cupertino.

If you would like to talk further about this piece or my career, please get in touch on LinkedIn or Twitter. You can also find previous reports on LinkedIn or remynuma.com.

There’s also never been so much good television to watch. Networks and streaming services are investing billions of dollars in high quality, critically acclaimed television to secure not just casual viewers, but paying subscribers in a post-cable environment.

It’s therefore crucial to examine the prestige TV landscape in some depth. Companies should know which TV shows are performing best, and the creative and industry trends that will help shape next year’s best programming.

I’m very interested in helping figure out the future of television. So, as 2018 ends, and with no university until March, I’ve prepared a simple report analysing these issues.

As the title says, this is a rough, back-of-the-envelope analysis. I’ve mentioned the key limitations below, and you may find others. Nonetheless, this piece at least serves as a shortcut through having to read every ‘best TV’ list put out by a major publication, and it’s a useful starting point to discuss out the industry’s future.

Finally, a disclosure: I’ve previously worked for 21st Century Fox and NBCUniversal. This report only uses publicly available information, and the analysis/opinions expressed are mine.

Methodology

FX’s annual scripted series report is the gold standard of TV industry analysis, so you should look at their research for an overview of the television landscape (I couldn’t find any full PDFs, but this year’s key charts are everywhere, as are scraps of previous reports).

This is a simple tally. I searched online for ‘best TV’ lists, read them, added series as they appeared on the lists, then totalled and ranked each series. I excluded outliers (i.e. series which appeared only once) from the analysis.

I included publications which met this criteria:

Notable following (at least 10,000 followers on Twitter). I excluded personal blogs and Twitter threads.

US-based (there are lots of great international TV critics, and I’d be here forever if I tallied all their lists too).

List published any time between December 1 and December 26.

A simple year-end ‘best of TV’ list. Some outlets also published lists by genre, streaming service availability, whether it first aired in 2018, and/or some other factor. Others published inventive but unquantifiable lists. They are worth reading but were excluded.

I also excluded lists with more than 50 series.

I’ve included links to each of the 42 included publications at the end of this piece. If I missed one that meets the criteria, let me know.

Limitations

There are several, including but not limited to:

The tally only examines the ‘best’ TV of the year, as judged by U.S. TV critics who publish year-end lists.

Critics have divergent opinions on what constitutes the ‘best,’ (e.g. Todd VanDerWerff’s “7 great shows” vs Tim Goodman’s “32 best shows”), but since every series on every list gets counted, the critics who were less discriminating have more influence on the final score.

Some critics are better and/or more influential than others, but every list was given the same weighting.

Some critics included stand-up specials, TV movies, and/or unscripted television in their lists, but most didn’t.

1. The best shows of the year, according to 42 professional television critics

Starting with the 10 shows which appeared on the highest number of year-end lists. I’ve included the title, U.S. premiere network, and the number of lists (out of 42) on which each show appeared.

Top 10

1. Killing Eve |BBC America | 37 lists 2. Atlanta |FX | 35 lists 3. Succession |HBO | 26 lists 4. The Americans (tie) | FX | 25 lists 4. Barry (tie)| HBO | 25 lists 6. The Good Place | NBC | 24 lists 7. Homecoming | Prime Video | 23 lists 8. Pose | FX | 22 lists 9. American Crime Story: Versace (tie)| FX | 18 lists 9. Better Call Saul (tie) | AMC | 18 lists

Appeared on at least 4 lists, in descending order

A lot of tied places from this point onwards.

10. Sharp Objects | HBO | 17 lists 11. BoJack Horseman | Netflix | 16 lists 11. GLOW | Netflix | 16 lists 11. Queer Eye | Netflix | 16 lists 14. The Good Fight | CBS All Access | 15 lists 15. Big Mouth | Netflix | 14 lists 16. The Marvelous Mrs Maisel | Prime Video | 12 lists 16. One Day at a Time | Netflix | 12 lists 18. Brooklyn Nine-Nine | FOX | 11 lists 18. My Brilliant Friend | HBO | 11 lists 20. American Vandal | Netflix | 10 lists 20. The End of the F–ing World | Netflix | 10 lists 22. Dear White People | Netflix | 9 lists 22. The Haunting of Hill House | Netflix | 9 lists 22. High Maintenance | HBO | 9 lists 22. You | Lifetime | 9 lists 26. Counterpart | Starz | 8 lists 26. Forever | Prime Video | 8 lists 26. Lodge 49 | AMC | 8 lists 26. Maniac | Netflix | 8 lists 26. A Very English Scandal | Prime Video | 8 lists 30. Howard’s End | Starz | 7 lists 30. The Little Drummer Girl | AMC | 7 lists 30. Patrick Melrose | Showtime | 7 lists 30. Sorry For Your Loss | Facebook Watch | 7 lists 30. The Terror | AMC | 7 lists 35. Babylon Berlin | Netflix | 6 lists 35. Cobra Kai | YouTube | 6 lists 35. Crazy Ex-Girlfriend | The CW | 6 lists 35. The Deuce | HBO | 6 lists 35. Jane the Virgin | The CW | 6 lists 35. Random Acts of Flyness | HBO | 6 lists 41. Billions | Showtime | 5 lists 41. The Handmaid’s Tale | Hulu | 5 lists 41. Schitt’s Creek | Pop | 5 lists 41. Wild Wild Country | Netflix | 5 lists 45. America to Me | Starz | 4 lists 45. Bodyguard | Netflix | 4 lists 45. The Chilling Adventures of Sabrina | Netflix | 4 lists 45. DC’s Legends of Tomorrow | The CW | 4 lists 45. Escape at Dannemora | Showtime | 4 lists 45. The Great British Baking Show | Netflix | 4 lists 45. Insecure | HBO | 4 lists 45. Kidding | Showtime | 4 lists 45. Salt, Fat, Acid, Heat | Netflix | 4 lists 45. Superstore | NBC | 4 lists 45. Vida | Starz | 4 lists 45. Westworld | HBO | 4 lists

Appeared on 2-3 lists, in alphabetical order

Adventure Time, American Horror Story, The Bisexual, Blue Planet II, Bob’s Burgers, Casual, The Chi, Claws, Corporate, Detectorists, Doctor Who, Elite, Everything Sucks!, Grown-ish, The Kids are Alright, The Kominsky Method, Legion, Nanette, Outlander, Summer Camp Island, This Close, This Is Us, Trial & Error, The Zen Diaries of Garry Shandling

Full list

You can download a full list here,which includes outlier shows and the publication/s where each show appeared.

2. Creative trends

Darkness prevails

Prestige television is still very dark. Critics praised grittiness, cruelty, and bleakness in their evaluations of the year’s best television. “A nasty and delicious dark comedy” (Succession) led Emily Nussbaum’s list of recommendations, while Matt Zoller Seitz praised shows with a focus on “resentment, fear, and anguish” (GLOW). Reviewers didn’t look for darkness for darkness’ sake – there’s plenty of bleak television that didn’t make the cut – but dark shows were ubiquitous.

It’s hard to spot dominant themes, but among the top ten, three of the most loved shows of the year (Killing Eve, Barry, and ACS: Versace) featured murderers as their lead characters, while the most popular comedy, Atlanta, is a meditation on racial inequality, drugs, violence, and poverty. Other popular issues included depression (BoJack Horseman, Maniac, Kidding) and domestic abuse (Sharp Objects, The Good Fight, Patrick Melrose).

The cheeriest show on the list is The Good Place (#6), which Alex McLevy called “a respite from the cruelty and coldness too often running through not just real life, but the rest of the TV landscape”. Other bright spots include Queer Eye (#11), Jane the Virgin (#35), and the relentlessly warm Great British Baking Show (#45).

Critics prioritised originality

Critics rewarded series with original plots, characters, and settings. Half of the top ten series first premiered in 2018 (six if you include anthology series American Crime Story), and across the board, critics singled out shows with inventive storytelling. Standouts in this area included My Brilliant Friend (#18), The End of the F–ing World (#20), Lodge 49 (#26), Maniac (#26), and Counterpart (#26).

Superhero shows struggled: only DC’s Legends of Tomorrow (#45) and Legion made the list, while Netflix’s Marvel-based series were ignored (including previous hit Jessica Jones). Prime Video’s blockbuster action seriesJack Ryan, based on the movie franchise, was also left off.

To find critical success for ‘franchises,’ you have to get creative. You could argue that Better Call Saul is successful because of Breaking Bad, Ryan Murphy is a household name, and Saturday Night Live alumni show up everywhere (this year, in Barry, Brooklyn Nine-Nine, and Forever).

Multi-cam sitcoms are critical poison

People like to divide television comedy into single-cam and multi-cam, but that puts an optimistic network comedy like Superstore in the same category as HBO’s dark hitman dramedy Barry. I think this three category approach is better:

Traditional/multi-cam sitcoms are on the left of the continuum, dramedy on the right. Lighter single-camera comedies are in the middle. He’s not the only creator working in this middle space (pioneers include Tina Fey, Liz Meriwether, and Kenya Barris) but since he’s got two shows high on the list this year, let’s call these Schur-coms.

92% of the comedies on critics’ lists were Schur-coms and dramedies. Schur’s The Good Place and Brooklyn Nine-Nine did great in that middle category, while Atlanta, Barry, and GLOW did well in dramedy. Within the 92% total, 27% were Schur-coms and 65% were dramedies, so much like the other genres, the darker you get, the more critics generally seem to like it.

If you’re looking for critical praise, you don’t want to be in the multi-cam business. The exception is Netflix’s Latino family sitcom One Day at a Time (#16). Ratings hits like The Big Bang Theory and The Connorsdidn’t make the list, and new entries like The Neighborhood didn’t show up either.

Prestige TV stayed away from political settings

U.S. political shows were absent. None of the top 60 above featured U.S. politicians as lead characters, none featured an election campaign as the central plot line, and none were set in political environments. (A Very English Scandal and Bodyguard are the exceptions, but both are British imports.)

I suspect the logic is that in a divisive America, it doesn’t make sense to split your audience in half. That adds up in a network TV environment, but given prestige TV mostly exists on cable and streaming services, and there’s plenty of left-leaning drama and comedy on the list, the lack of strictly political television this year is surprising.

The gap might also be a result of discomfort in the creative community. Showrunners have grappled publicly with the idea of writing political characters in the Trump era. Some, like Homeland’s Alex Gansa, see “more and more of a responsibility to comment on it”, while the creators of Broad City, Curb Your Enthusiasm, Insecure, and Master of None have gone out of their way to avoid mentioning the current administration on their shows.

Finally, two of the heaviest hitters in political television, House of Cards and Veep, were both absent. The rewritten final season of House of Cards debuted to mixed reviews, and Veep was delayed until 2019 due to Julia Louis-Dreyfus’ cancer diagnosis.

To be clear: television was very political this year. Even among the top ten shows, economic inequality, war, race relations, feminism, and foreign diplomacy played strong roles, and that list of issues expands as you look further down the list. The point here is that everyone wanted to talk about politics, just not in a political setting.

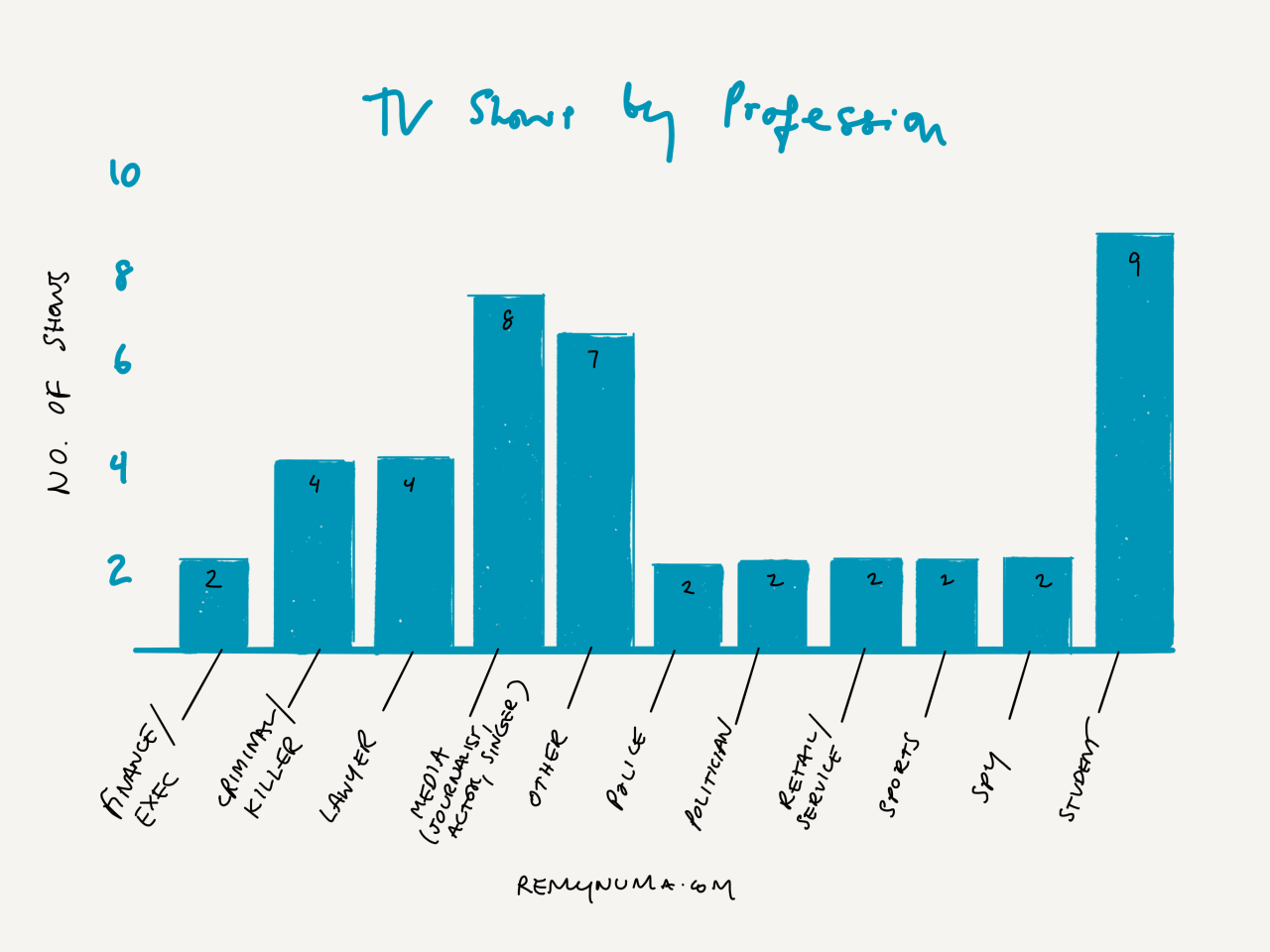

Lots of shows about students and the media, but other professions mostly unrepresented

Shows with a focus on professional/career issues made up just over half of prestige television series in 2018 at about 57%. The other 43% mostly focused on families, and a handful had a sci-fi/horror setting.

Among career-focused shows, it was a mixed bag for the leading professions:

Nine featuring high school and/or college students were well reviewed. The biggest successes were American Vandal, The End of the F–ing World, and Dear White People, all three of which premiered on Netflix. In fact, six out of the nine student shows altogether were Netflix exclusives (the other three were Sabrina, Elite, and Everything Sucks!). The other youth networks didn’t fare great, but Freeform made an appearance with Grown-ish.

The industry also continues to look inward for inspiration. Succession focused on media dynasties, Jim Carrey played a TV host in Kidding, and BoJack Horseman is set in Hollywoo(d). Other media-based shows involved journalists (Sharp Objects), comedians (Maisel), music (Atlanta), and the adult industry (The Deuce).

Tough break for doctors, and slim pickings for working-class Americans looking for shows about their jobs. A handful of critics rooted for Superstore and Bob’s Burgers, but large sections of the population remain unrepresented.

A great year for the UK and foreign languages

Raise a glass for our friends in the UK. Killing Eve was the single best TV show of the year according to critics, appearing on 88% of all lists. Other UK productions included The End of the F–ing World (#20), A Very English Scandal (26), Howard’s End (#30), The Little Drummer Girl (#30), Patrick Melrose (#30), Bodyguard (#45), The Great British Baking Show (#45), plus The Bisexual, Detectorists, and Doctor Who.

A breakthrough year for non-English speaking television too. HBO aired its first captioned series with My Brilliant Friend, a co-production with Italy’s RAI Network. The show landed on 11 critics’ lists, above several of HBO’s higher-profile English speaking productions. Netflix also won with Germany’s Babylon Berlin (which was available dubbed or with captions).

American critics lacked an appetite for shows from other countries.

The year of the woman, but no parity

Female-led scripted television did well in 2018. Killing Eve is the headline again, with Jodie Comer and Sandra Oh in leading roles (Oh was also the first Asian woman to receive a lead actress Emmy nomination). Critics also singled out the feminist themes and casts in Pose (#8), Sharp Objects (#10) and GLOW (#11). Amazon’s hit The Marvelous Mrs Maisel had notable detractors, but still did well at #16.

There’s still work to be done: by my count, 35% of the leading actors in the top 10 shows of 2018 identified as women. It would be better to look at screen time (e.g. men make up the majority of the nine-person Killing Eve cast, even though Comer/Oh dominate), but no parity yet.

Nonetheless, in male-led and ensemble shows, critics tended to single out female performers. Standouts included Zazie Beets (Atlanta), Keri Russell (The Americans), and Kristen Bell (The Good Place).

And just out of the top five, two renowned female movie stars made their television debut: Julia Roberts (Homecoming) and Amy Adams (Sharp Objects).

Progress on racial equality

White performers made up the majority of the cast in 6 out of the top 10 shows of the year. Half of The Good Place’s leading cast is white, while Atlanta was majority black, Pose was majority black and Latino, and Versace was majority Latino. Again, screen time is a better metric to use.

Black representation can be found across the rest of the best-received shows of the year. Fox’s Brooklyn Nine-Nine is one of the few network sitcoms with more than one black lead, and critics also praised black scripted television in Netflix’s Dear White People (#22) and HBO’s Insecure (#45). Further down, The Chi and Grown-ish also appeared on multiple lists.

Across the full list of shows, the Latino community was represented most prominently in Netflix’s One Day at a Time (#16), The CW’s Jane the Virgin (#35), and Starz’ new entry Vida (#45). While Latino performers played parts in many of the top 60 shows above, Versace’s Édgar Ramírez, Ricky Martin, and Penélope Cruz got the most attention.

This is by no means comprehensive. I focused on black and Latino casts, since they are the two largest minority groups in America, but I also found little representation of Asian Americans (Killing Eve and The Good Place have one lead Asian performer each), and I’m struggling to find Native American representation at all in the top 10 shows.

LGBT representation pushed forward, especially by Ryan Murphy

Ryan Murphy is a man on a mission to increase LGBT visibility. Between his and FX’s Versace and Pose, LGBT characters led two out of the top 10 series of the year. Netflix’s Queer Eye came in just below, appearing on 16 lists (impressive, given several critics only included scripted shows). Netflix will do better once Murphy sets up shop there.

Divergence between Emmy voters and critics

Finally, Emmys voters and critics continue to disagree about the best shows of the year. In drama, Emmy nominees for series released in 2018 includedThe Handmaid’s Tale, This is Us, and Westworld, none of which cracked the top 25 on critics’ lists, while critics’ top pick, Killing Eve, failed to secure a Best Drama nomination. In comedy, Emmy nominees includedBlack-ish, Silicon Valley, and Unbreakable Kimmy Schmidt, which also failed to crack critics’ top 25. Critics’ top selection, Atlanta, made it into the Emmy nominations for Best Comedy, but voters favored The Marvelous Mrs Maisel.

3. Industry trends

Let’s start by breaking down the number of shows by platform:1

You can see how difficult life is getting for the cable bundle. Streaming accounted for 39% of the top shows of the year, with another 12% for network television. When you add in the three premium networks, which represent 25% of the chart and which are now available as standalone SVOD services, you can watch ~75% of the year’s best television without a cable subscription.

That 25% basic cable segment will likely shrink again next year, given Disney, Warner, and Apple will all enter the streaming market. From a scripted entertainment perspective, I can’t see a viable future for this platform.

Critics mostly ignored network television

The networks aired 146 original series in 2018, and 10 of those made it on to critics’ year-end lists. That’s just under 7%. Critics were particularly harsh on network drama/procedural series: of the big 4 networks, only NBC’s This Is Us made it on to the list. Comedy fared better, but critics ignored CBS’ top-rated comedies, and only rewarded a handful of sitcoms overall.

NBC was the strongest performer with four shows, and the only network to crack the top 25 with The Good Place (#6). The CW had three middling entries: Jane the Virgin (#35), DC’s Legends of Tomorrow (#45) and Crazy Ex-Girlfriend. Fox was best represented by Brooklyn Nine-Nine (#18), ABC just made it in with The Kids are Alright, and CBS had nothing.

Fox cleared house in 2018, leaving it without critical darlings New Girl and The Last Man on Earth to shore up its figures (neither were included on lists this year, but made multiple appearances over the past decade). It triumphed with Brooklyn Nine-Nine, which moves to NBC in January. Many of its new arrivals are performing well with viewers (Last Man Standing is a hit), but as it makes more room in the schedule for sports and event programming, it’ll be tougher to please critics.

FX and AMC dominated basic cable

The man who coined ‘Peak TV’ plays an outsized role in creating it. FX had six shows on the list in 2018, including 4 out of the top 10 (Atlanta, The Americans, Pose, and Versace). When Disney acquires the network in early 2019, John Landgraf will remain as its head, so expect to see more praise for FX even as its business model shifts.

AMC Networks had seven shows altogether. Four aired on AMC (Better Call Saul, Lodge 49, The Little Drummer Girl, and The Terror), with another three on AMC’s majority-owned BBC America (Killing Eve, Doctor Who, and Blue Planet II). Four out of the seven were either created by or with the BBC.

Executives at NBCU, Turner, and Viacom will be less pleased. All three own networks in the prestige TV business (USA, TNT, and Paramount, respectively), but only TNT made the list, with Claws. All three networks had solid contenders, with USA’s The Sinner, TNT’s The Alienist and Paramount’s Yellowstone all performing well with viewers. Given that Paramount relaunched this year with five original series and a splashy campaign, Viacom has to be feeling particularly frustrated. These basic cable networks suffered because the landscape is too cluttered.

All three premium networks have something to offer, but HBO leads

HBO continues to lead the premium cable networks, with 10 shows on the list, including 2 of the top 10. Succession (#3) and Barry (#4) played best with critics, followed closely by Sharp Objects (#10) and My Brilliant Friend (#18), but the network has shows scattered throughout the list. HBO currently charges standalone subscribers $15 per month for its service (versus $11 for Showtime and $9 for Starz), and in 2018, it offered twice as much prestige TV as the other two networks for that price.

Showtime and Starz each had five shows on the list. Showtime’s best performers included Patrick Melrose, Billions, Escape at Dannemora, Kidding, and The Chi, while Starz found success with Counterpart, Howard’s End, America to Me, Vida, and Outlander. Neither network cracked the top 25.

Netflix wins on volume

Netflix offered viewers 20 shows on this list in 2018, by far the highest number of shows from any single network. BoJack Horseman (#11), GLOW (#11), Queer Eye (#11), Big Mouth (#15), One Day at a Time (#16), American Vandal (#20), The End of the F–ing World (#20), Dear White People (#22), and The Haunting of Hill House (#22) all cracked the top 25.

Industry observers point out that Netflix makes a lot of very good television, but they’re yet to make the best television. That’s reflected in this year’s list, where none of Netflix’s shows made it into the top 10. They’re also yet to win an Emmy for Best Drama or Comedy series.

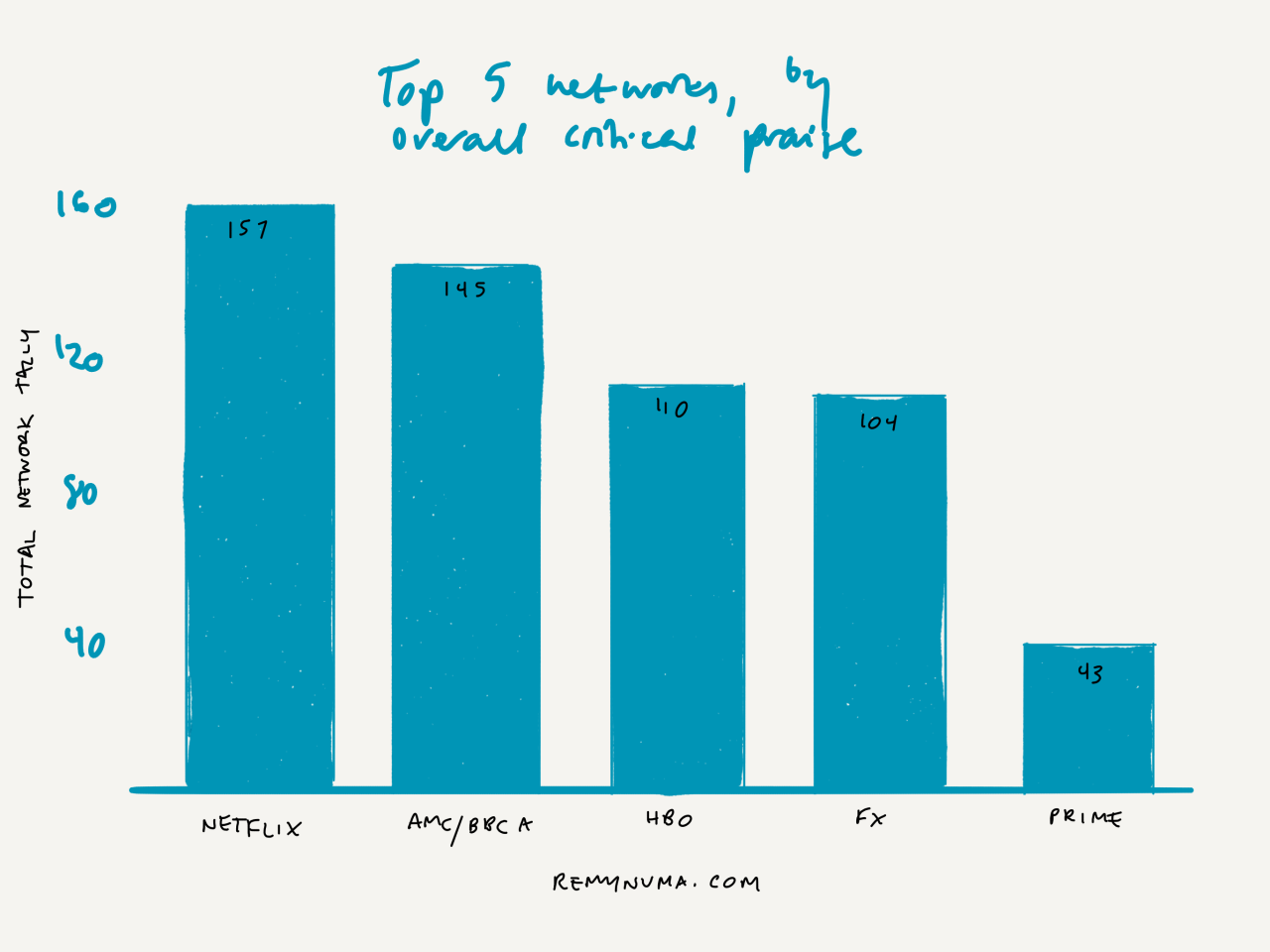

I don’t think that matters to anyone outside of the TV critic community. When you measure the top five networks by the number of shows they offer andthe extent to which each critic liked those shows, Netflix still wins:

Any reasonable person looking at that chart would conclude that Netflix is doing the best job at entertaining them, all in one neat ~$10 payment. Plus, Netflix has both the scale and technology to target those shows at the viewers most likely to watch them.

Turning to the rest of the streamers, Prime Video barely made it into the top five networks by critical weight. They only had four shows on the list, but critics ranked them highly, with Homecoming (#7), Maisel (#16), Forever (#26), and A Very English Scandal (#26).

Bad news for Hulu, which struggled after mixed reviews for the second season of The Handmaid’s Tale. That show made the list, but only at #41. UK import The Bisexual and the recently canceled Casual were the only others to make it.

Disney and Warner will launch with experience

When Apple, Disney, and Warner launch new streaming products next year, you can expect some of their original series to show up here. But it will be significantly harder for Apple than it is for Disney (which will soon own FX) and Warner (which owns HBO and Turner), both of which already dominate among TV critics.

Prestige TV is already too expensive, and it will get worse without consolidation

Here’s the best value combination I could find to watch every show on the list:

$131 (or $139 without ads) is prohibitive for the vast majority of U.S. television viewers. According to one analytics firm, ~66% of Americans pay for one or zero streaming services, ~32% of Americans are willing to pay for at least two services, and only ~4% are willing to pay for more than four. To watch every show on the list, you need to subscribe to seven, plus cable with every premium network.

In its present form, the market is unsustainable, and that’s a big reason why the cable bundle will soon fall apart. But even when it does, viewers looking for a high quality entertainment will still have too many options. Let’s assume a post-cable environment where all the key players are fighting for viewers:

Streaming services (Netflix, Disney/Hulu, Prime Video, Apple, NBCU service, CBS All Access plus niche services e.g. Sundance Now)

Premium services (HBO, Showtime, Starz, Epix)

Other cable networks (A&E, AMC, Discovery, Viacom etc)

Sports (ESPN, NBCSN, Fox Sports)

News (Fox News/Nation, MSNBC, CNN)

That’s even less sustainable than today’s market.

Given the nightmare landscape above, I think Apple will distribute its original shows for free, rather than as a subscription service, when it launches next year. Apple’s already getting customers used to that method of distribution with season two of Carpool Karaoke, and while the company keeps signalling that it wants to build service revenue, it would also like to own the living room. Having more than 20 highly-anticipated scripted series, available for free and without ads, exclusively on Apple TV, is a good way to get there.

UK co-productions perform well

In the meantime, as cable and streaming services keep trying to reach the top of the leaderboard, UK co-productions are helping American networks get there. As noted above, the UK provided 10 of the year’s most critically acclaimed shows, and by my count, four of those were co-produced: Howard’s End (BBC/Starz), The Little Drummer Girl (BBC/AMC), Patrick Melrose (Sky Atlantic/Showtime), and Doctor Who (BBC/BBC America). The others were US rights purchases (mostly on Netflix).

Co-productions allow UK networks to air more original series – BBC’s The Night Manager, for example,would never have been greenlit without AMC’s financial support – and they lower the cost for US networks looking for a lavish production. You’ll keep seeing these next year.

Great TV doesn’t save a network

Finally, remember that this analysis is limited to critically acclaimed television. Every network mentioned here wants well-reviewed shows, and those reviews can make the difference between renewal and cancelation when it is otherwise a toss-up. But a popular show doesn’t need great reviews to bring in customers and/or viewers, and an unpopular show won’t survive just because The New York Times wrote about it. Lifetime learned that the hard way this year. The network made waves with UnReal in 2015, and appeared at #22 this year with You, but it still handed both shows off to streaming services (Hulu and Netflix, respectively) earlier this year.

The television industry has steadily increased its television output for nearly a decade now, and aside from its bloat, there isn’t anything especially striking about the landscape in 2018 versus the last two years. But it feels like we’re finally on the verge of a new landscape. When Disney and Warner enter the market next year, viewers around the US will start remaking their television budgets. As the analysis above shows, almost every major network/service feels they need to offer a wide range of prestige TV to survive.

Impressive start for Roseanne-sans-Roseanne last night. It’s a long way from the monster 18.2 million/5.1 rating from last year’s premiere, but just a tick down from the 10.5 million who watched the season finale in May.

What we don’t know: how many of those 10.4 million viewers are loyal Roseanne fans, and how many were sampling the show for the first time since the original series (or ever)?

Nathan Hubbard, a former Live Nation exec, on Taylor Swift’s record deal:

So it sounds like you’ll be surprised if there’s a story tomorrow that says she is re-upped for a four or two or whatever album deal with Universal and has got an X-sized advance and it kind of looks like any other artist deal?

If it looks like any other deal, I’ll be surprised. I wouldn’t be surprised if she continues the relationship with Universal. Great label, can support her in all kinds of ways. But I’m quite sure that she’ll have some interesting control and independence in decision-making and maybe even in the way that she releases her content going forward. It seems to me silly to start doing record deals based on albums now. “You owe me an album. We’re gonna do a five album deal.” In a world in which streaming is blowing up that concept altogether, why would you do an album deal versus a content-focused deal?

Except that for a handful of people, and she’s one of them, people still buy her albums, they buy digital versions of her albums, they buy actual CDs.

Of course, I’d just argue that she could probably make as much as she’s getting paid for one-eighth of the content. And that it’s probably in her business interest to — just like sports leagues divvy up their media rights and sell them — that she can divvy up her content rights and make more money in the aggregate because each individual Taylor Swift song is probably worth more than the sum of the parts.

Price discrimination works for Swift, so I can’t see that changing under a new deal. The rest, as Hubbard argues, is up for negotiation.

Former White House communications director and longtime Donald Trump aide Hope Hicks has been named executive vp and chief communications officer of the new Fox company.